Keypoints

- Pricing pressure on cars in 2024

- A lot of dealerships closing. What’s going on?

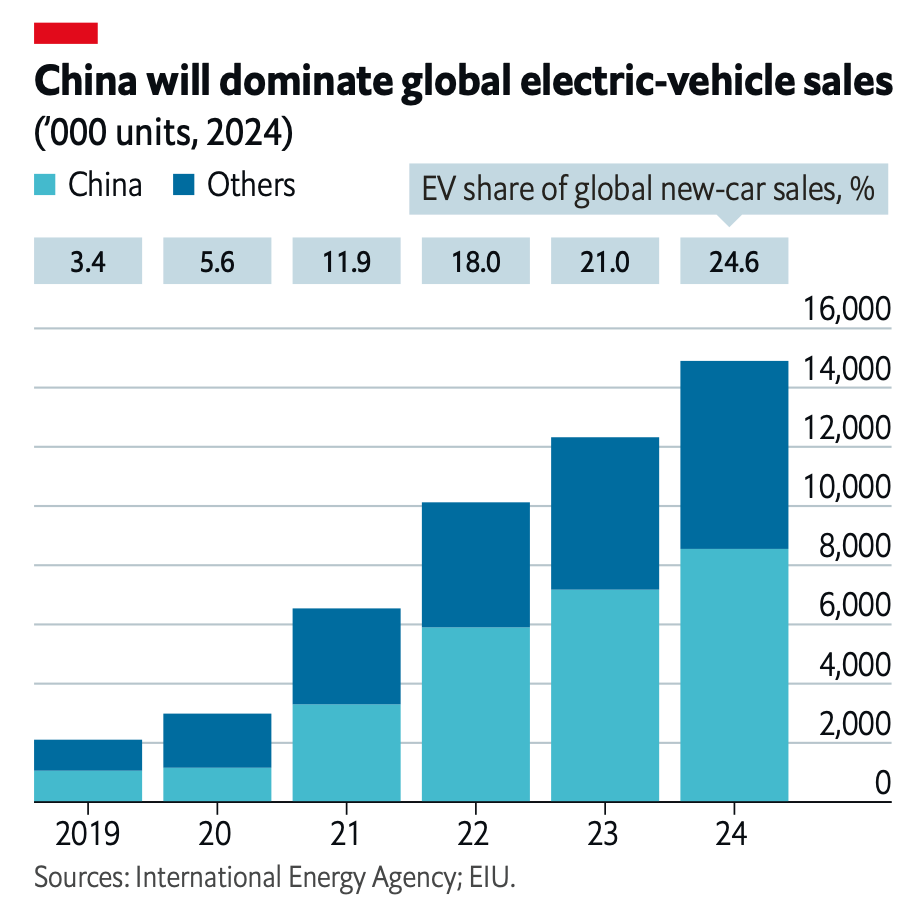

- China will account for more than half of global EV sales

- Emissions legislation will tighten further, with many cities introducing clean-air regulations that will affect vehicle usage.

The automotive industry will face another subdued year in 2024, weighed down by slow consumer spending, high interest rates and disruption to supply chains due to geopolitical tensions.

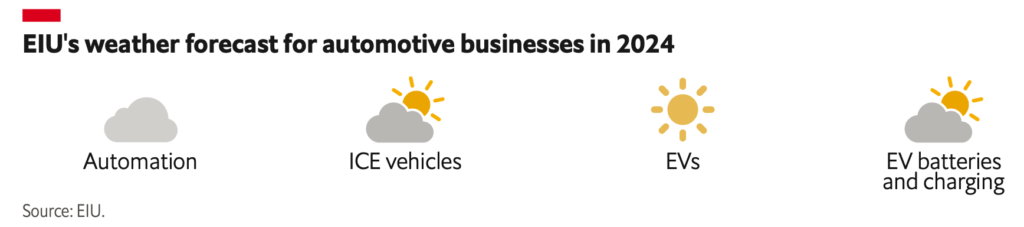

The only bright spot will be the electric vehicles market, with sales expected to soar by 21% as governments and consumers try to mitigate the worsening effects of climate change.

Pricing Pressure and Industry Challenges

The automotive industry is anticipated to face a challenging year in 2024, influenced by factors like slow consumer spending, high interest rates, and supply chain disruptions due to geopolitical strains.

Despite overall challenges, the electric vehicle (EV) market is expected to grow by 21%, driven by efforts to address climate change and governmental support.

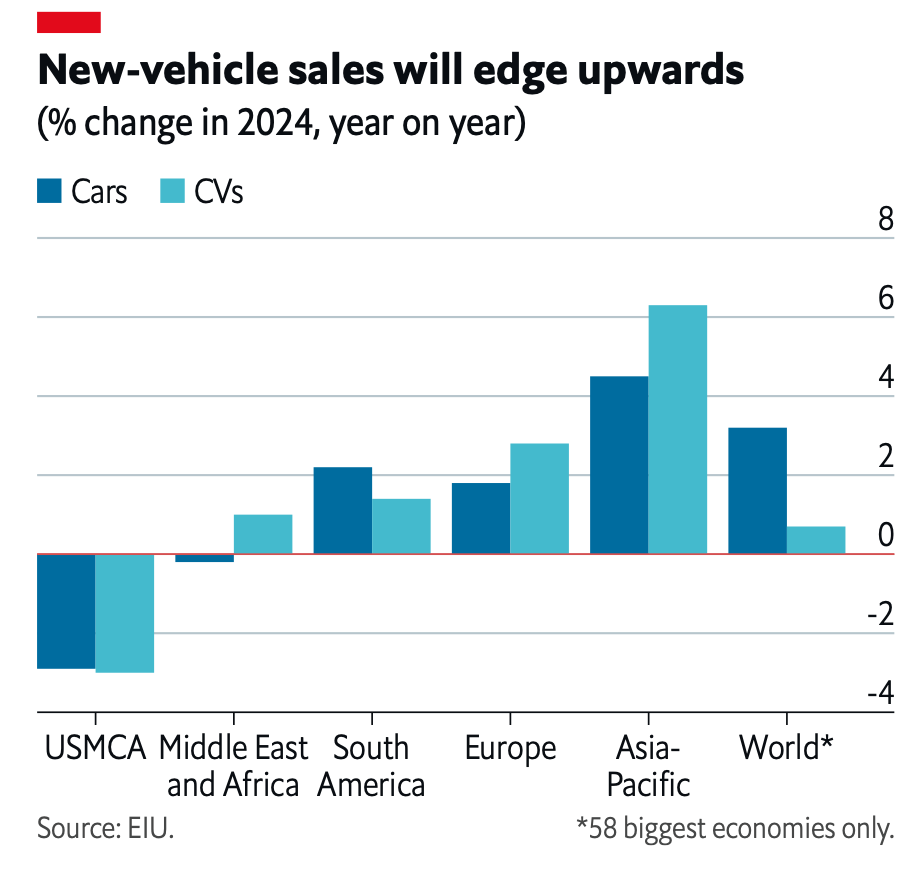

- A moderate increase in sales is expected, with passenger cars rising by 3% and commercial vehicles and buses by 1%.

- However, some auto companies are offering 0% for some of their models.

- This incentive will hike up sales exclusively in Q124, considering how Fed rates are crazy high now due to inflation.

Used car dealerships are closing down, is it an omen?

Interestingly, no! Used car dealerships are closing down, for a good reason.

- These are strategic closures, and the market is cleansing.

- The automotive market is undergoing an adjustment phase and will lead to a healthier, and more efficient outlook in the future, and it may involve more closures, mergers, or acquisitions in the short term.

- Of course, slow economic growth and high-interest rates are creating financial pressures on dealerships. These conditions make it more challenging for consumers to finance new vehicle purchases, impacting dealership sales.

- Consumer preferences are evolving, with a notable trend towards online buying. Dealerships are closing down because less foot traffic. They are adapting to this change, shifting more towards digital sales.

- People are buying more Teslas, as they have found it to be more cost efficient in the long run, with all the incentives offered.

- Rising popularity of EVs is reshaping the market. Dealerships need to adapt to this trend, which might involve significant changes in inventory and sales strategies.

The automotive market is still looking good for 2024, especially in the EV department since more and more consumers are shifting preferences.

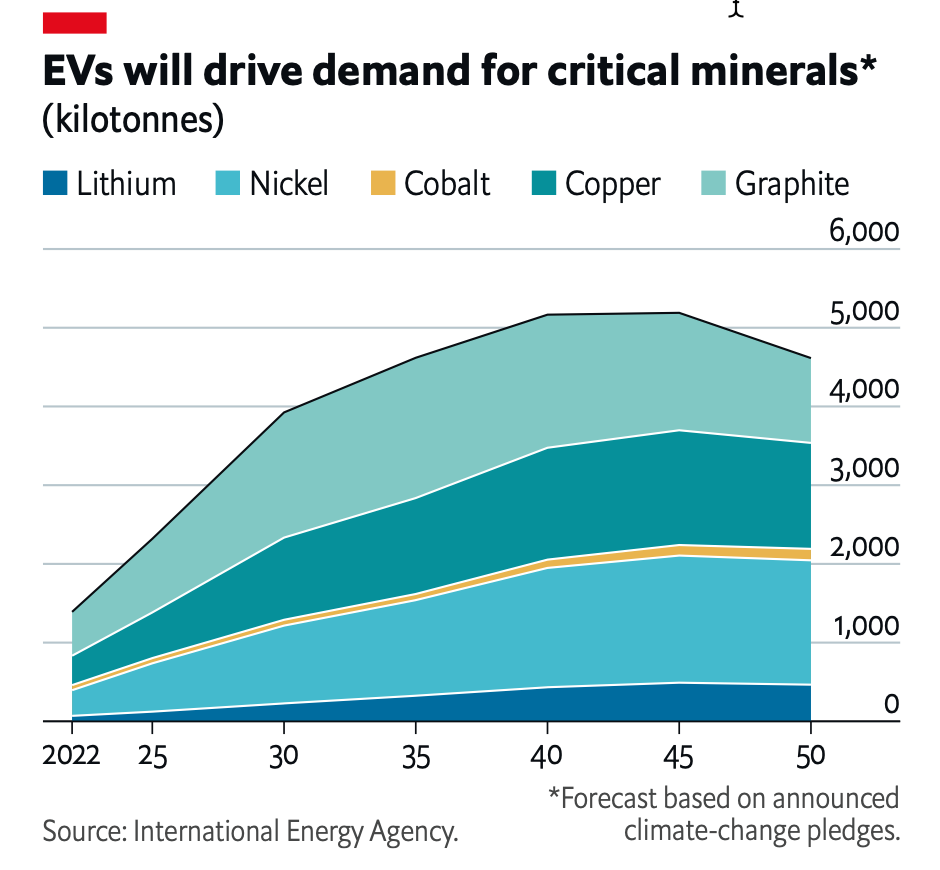

Better EV batteries in 2024

- Companies are investing in battery material supply through direct investments, long-term agreements, and recycling initiatives.

- Automakers are focusing on easing range anxiety through new battery technologies, fast-charging stations, and charging standards.

- 2024 will witness the emergence of new EV battery technologies aimed at enhancing range, reducing charging times, and improving safety standards.

- The North American Charging Standard (NACS), developed by Tesla, is expected to become widespread in North America, contrasting Europe’s reliance on the Combined Charging System (CCS).

- Progress on EV and emission-related legislation in the US is expected to be slow, particularly with the contrasting political stances in the presidential election run-up.

China in EV’s driver’s seat

- China’s dominance in EV sales and exports will be a critical factor to watch, potentially stirring trade tensions due to its governmental backing.

Economic Indicators and Auto Market Sentiments

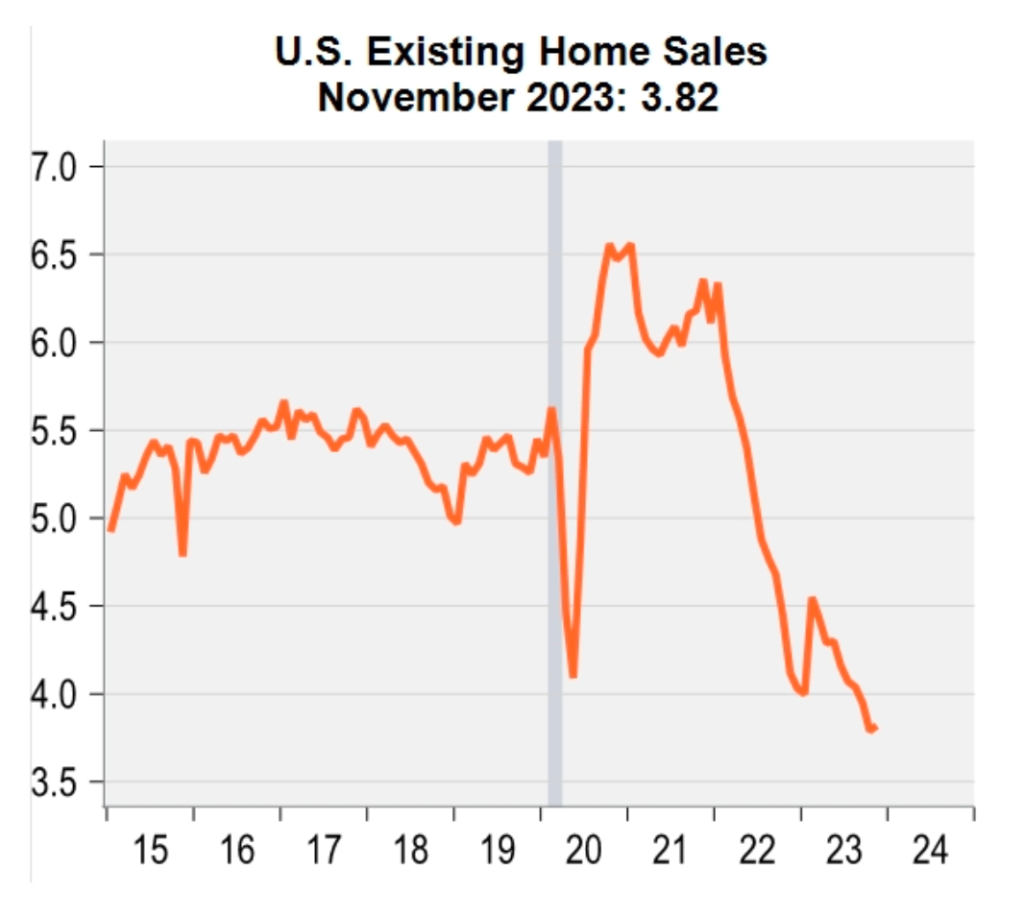

- The housing market’s gradual recovery and fluctuating consumer confidence present a complex picture for the economic and spending outlook.

- Existing house sales ticked up in November, following the November housing start surge.

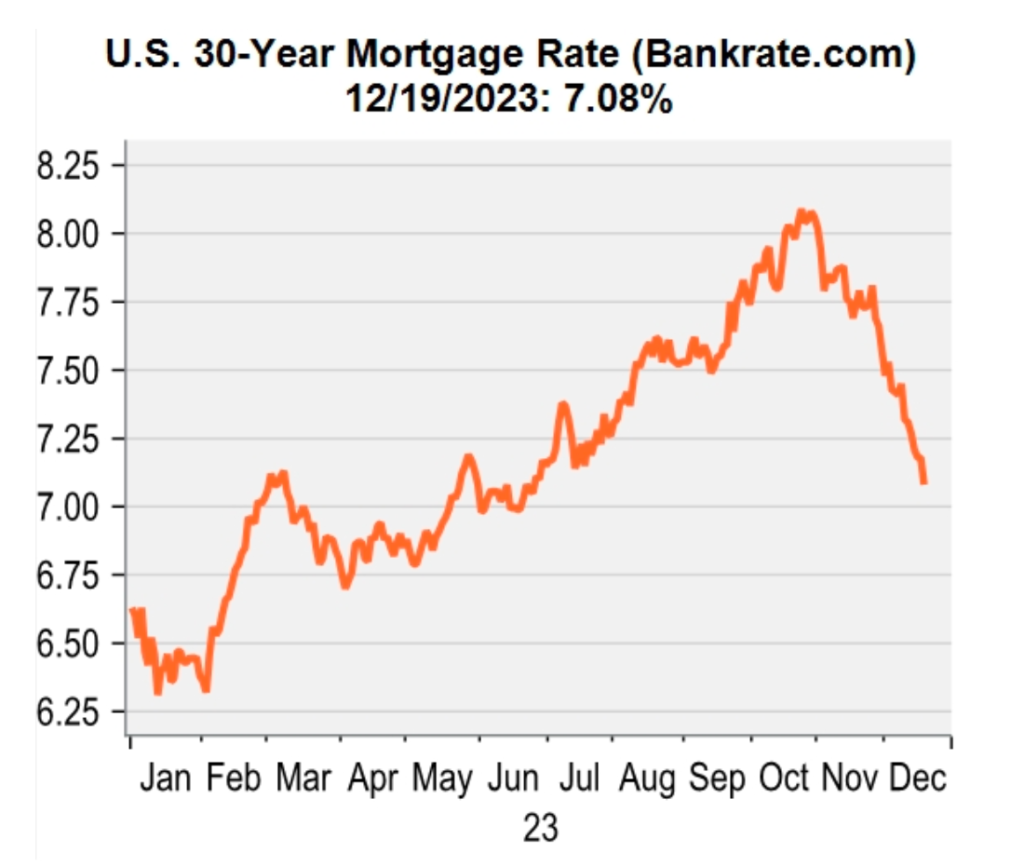

- Are lower mortgage rates helping? Probably not. They are still roughly 7%, with house prices egregiously high, keeping affordability very, very low.

- Housing expected to remain weak into 1H of 2024. Mortgage remain depressed.

- Market expectations lean towards early Federal Reserve rate cuts in 2024, a move that could significantly impact financial markets and consumer spending patterns.

- Consumer confidence has improved, helped by factors like higher stock prices and lower gas prices, yet future expectations remain low, indicating potential economic concerns.

- Housing market seems to be bottoming, and auto production and sales have picked up.

- Rates will most likely remain much higher next year than they were pre-Covid to get inflation under control.

- Extent of time for which rates are very elevated is crucial – determines how many households and businesses must borrow at those very high rates.

- Ultimately, it is all a bit circular: the reason that stocks are doing well and a recession is unlikely is that the Fed will probably cut rates any time soon.

- The unemployment rate is south of 4%, and wage inflation is north of 4%. That is a good setup for consumer spending.

Automotive forecast into Q124

- Implementation of the toughest ever vehicle emission standards in the US, passed by the Environmental Protection Agency in April 2023 has no definite timeline.

- EV government incentives will spike more EV cars on the road.

- So what to expect in 2024? Automotive emissions standards to support demand for newer vehicles, including EVs, but to dampen sales of second-hand vehicles.

- This may impact businesses involved in the resale and maintenance of older vehicles.

- More robotaxis on the road. The automotive industry will move faster towards adopting self-driving technology.

- Looking ahead to 2024, there are some risks, such as macroeconomic uncertainty, inflation, higher rates, weak consumer confidence, that all points to a potential U.S. recession.

- However, the forecast for 2024 is more constructive. After a SAAR of 13.7 million in 2022 and a trend of approximately 15.4 million SAAR in 2023, it is projected that auto sales will increase to 16.1 million in 2024

- The housing market’s recovery and improved consumer confidence, albeit with low future expectations, indicate mixed signals for economic outlook and consumer spending.

- Consumer resilience complicates Fed messaging – financial markets are anticipating a possible decrease in interest rates by the Federal Reserve as early as March 2024.

- Downside risks are: slower than expected revolving credit growth, faltering economic recovery and rising loan losses, which could drive earnings below our estimates, and result in valuation compression.

- Real disposable personal income ticked up 0.26% m/m, but is still below trend, a significant headwind to future spending.

The automotive industry in 2024 faces a complex landscape marked by economic, technological, and even political challenges. While the EV market shows promise, broader industry growth will be tempered by macroeconomic uncertainties and changing consumer behaviors. Technological advancements in EVs and changing legislative dynamics will play crucial roles in shaping the industry’s future. Stakeholders need to navigate these complexities with a focus on innovation, adaptability, and strategic foresight.