Last Updated on March 22, 2024 by inaz Ameera

January marks a cold start to 2024

The start of 2024 signals a nuanced phase for the U.S. automotive industry, with January’s sales data underscoring a cautiously optimistic yet challenging landscape. Here’s a closer look:

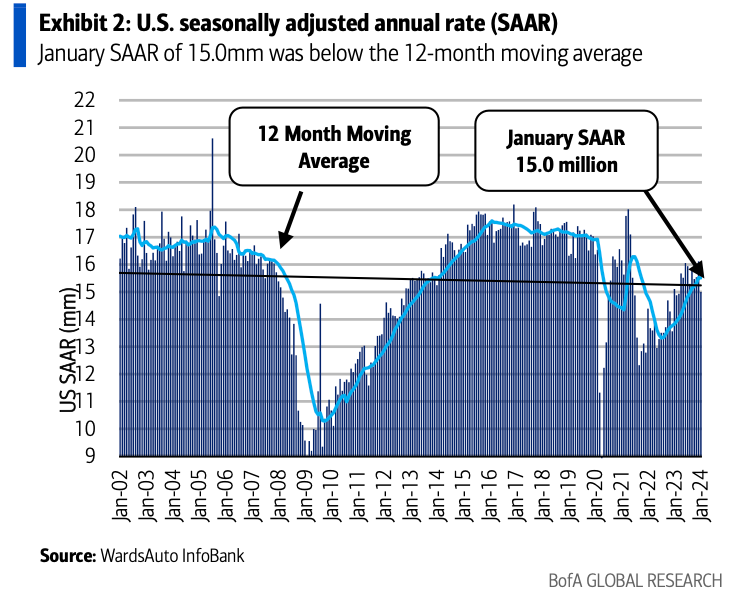

- The automotive sector witnessed a modest dip with a Seasonally Adjusted Annual Rate (SAAR) of 15.0 million units, falling short of expectations and marking a decrease from December’s 15.8 million SAAR.

- This was well below both estimate of 15.7mm and consensus of 15.7mm.

- January’s performance equates to an unadjusted volume increase of 2.8% YoY, but down -26% MoM from December 2023. We’d note that January is historically one of the smallest months of the year in terms of volume.

- In 2023, US sales grew solidly to 15.5mm (+12.5% YoY).

- Expected a further uptick in 2024 to 16.1mm (+4% YoY) and project sales will continue to build towards the next peak in the US auto cycle in 2028 (17-18mm range).

Inventory shrinking signalling to stronger sales

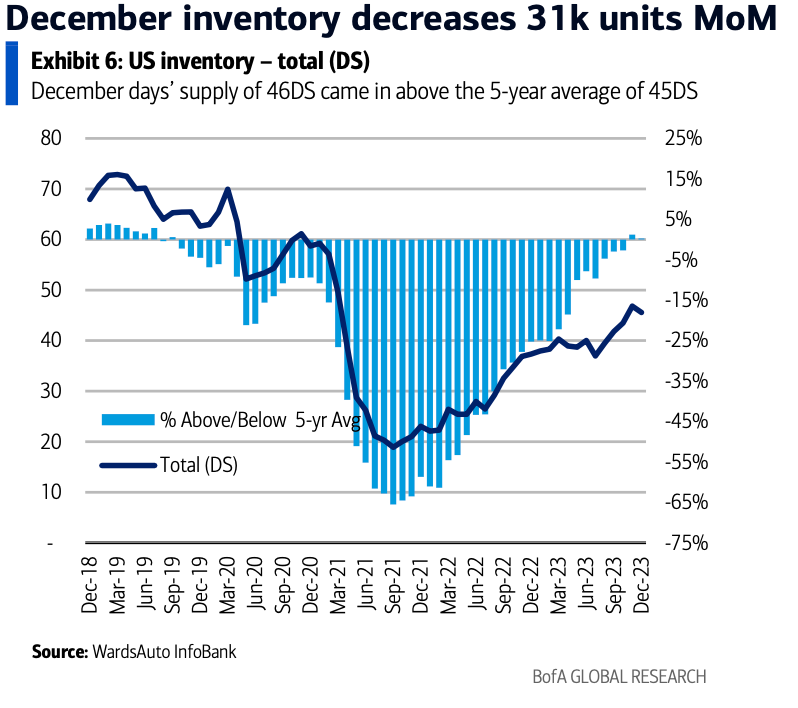

- Inventory levels contracted by 31,000 units from November to December 2023, indicative of strong sales but also highlighting a complex inventory landscape shaped by production adjustments and consumer demand shifts.

- The market share of light trucks and alternative powertrain vehicles continues to grow, reflecting evolving consumer preferences.

- However, average transaction prices saw a decrease, hinting at a potential rebalancing of pricing dynamics and consumer affordability concerns.

- With expectations of sales growth propelled by pent-up demand and a gradual inventory normalization, the industry remains poised for evolution.

- Almost all of the MoM decline in absolute inventory was driven by the Japanese (-42k) and Korean OEMs (-9k), while the D3 posted higher inventory (+14k), likely due to some restocking of models affected by the UAW strike in late 2023.

- Inventory for European OEMs grew (+6k). On a days’ supply (DS) basis, inventory stood at 46DS, which is a bit above the five-year average of 45DS, but down one day MoM.

- December inventory decline came in light of robust December sales, which were up MoM on a SAAR basis to 15.8mm

- Inventory remains somewhat lower than “normal” levels of 2.5mm-3.0mm+ units, but is gradually approaching this range.

- As production constraints faded in 2023, both sales and inventory started to recover after years in which low inventory impaired sales.

- Substantial unfulfilled demand following the last few years of shortages. Affordability could represent an obstacle for stronger demand to materialize.

- Yet, affordability and the pace of demand recovery, especially in the electric vehicle (EV) segment, remain pivotal factors to watch.

As we navigate through 2024, the automotive sector’s trajectory will be closely tied to broader economic indicators, consumer confidence, and technological advancements. The industry’s ability to adapt to these dynamics will be critical in steering towards sustainable growth and resilience in the face of ongoing challenges.

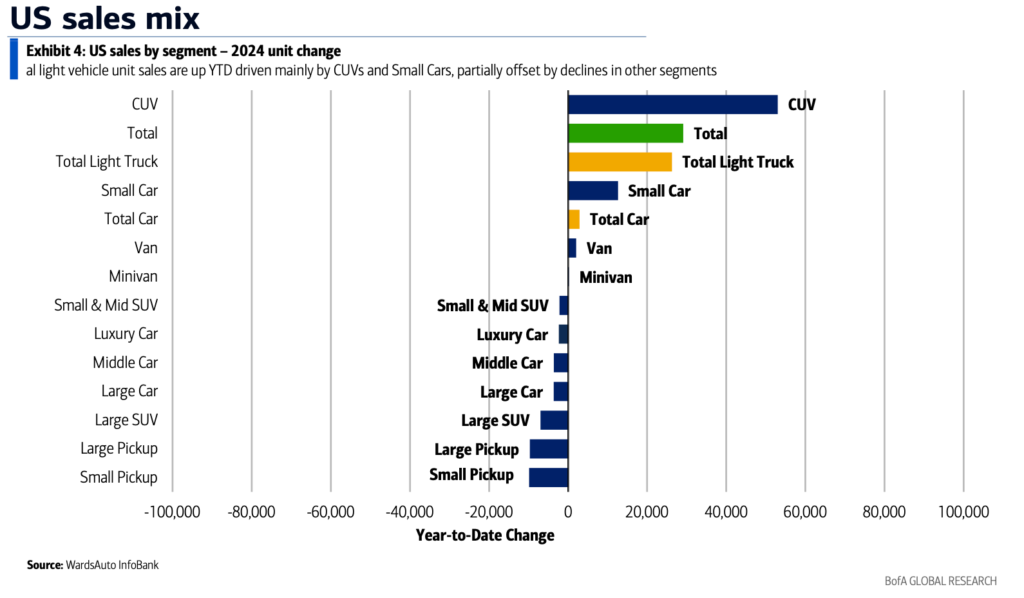

- Two data points that speak to the strength of underlying demand are mix and price, which remain near record levels.

- Light trucks (pickups, Sports Utility Vehicles (SUVs), Crossover Utility Vehicles (CUVs)) gained +140bps of market share relative to passenger cars in December on a YoY basis, while alternative powertrain vehicles gained +480bps from ICE vehicles YoY.

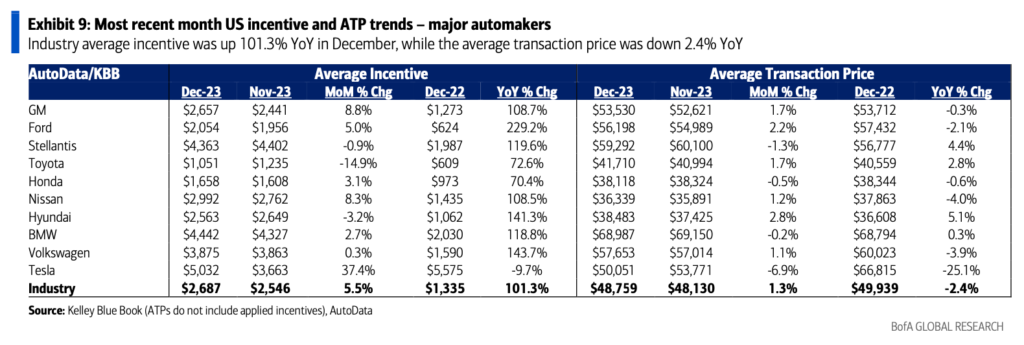

- Average transaction prices (ATPs) fell in December, down 2.4% YoY to $48,759 (-$1,180/unit YoY) but were +1.3% MoM according to Kelley Blue Book.

- Incentives were up 101% YoY and +6% MoM in December but are still well below 2019 levels (5.5% of ATP vs. ~10% in 2019).

- Insight → strong pricing trends (more transitory) and favorable mix shift that has occurred in the last 10 years (more structural) could begin to flatten out or fade as volumes begin to recover in the mid-2020s.

What’s Up Elon Musk?

- As of the most recent update, Tesla’s stock price was down 1.8% for the month, with a closing price of $185.10 the day before the last update and a latest price of $189.27

- Cox Automotive’s Electric Vehicle Sales Report stated that Tesla’s market share has fallen to 50%, which is the lowest on record, and down from nearly 65% in the same quarter last year.

- Reuters reports that registrations of Tesla vehicles in California dropped 10 percent in the last quarter of 2023.

- That is the first time sales of Tesla automobiles have fallen in the Golden State, which is ground zero for the EV revolution in the United States, in the past three years.

- Electric vehicle (EV) sales in the United States jumped to more than 300,000 for the first time in the third quarter, Tesla’s market share slipped to the lowest on record.

- Tesla now dominates just half of the market, down from the 62% it held in the first quarter.

- Tesla’s market share has declined due to a combination of factors, including increased competition as more automakers launch electric vehicles.

- This shift reflects the broader EV market’s expansion, with new entrants reducing Tesla’s dominance.

- Additionally, Tesla’s performance and strategy adjustments may also play a role, as the automotive sector evolves rapidly with technological advancements and consumer preferences shift.

- Elon Musk has publicly acknowledged that Tesla’s sales growth is expected to slow down, despite recent price cuts that have already impacted the company’s profit margins.

- He pointed out that Tesla’s focus is on developing a cheaper, next-generation electric vehicle to be produced at its Texas factory in the second half of 2025, aiming for a future boost in deliveries.

- However, Musk also noted the challenges in ramping up production for this new model due to its reliance on cutting-edge technologies.

- This acknowledgment came amid Tesla’s stock experiencing a significant drop, marking its sharpest intraday percentage loss in over a year, which contributed to a substantial decrease in its market valuation.

- Despite Tesla’s declining market share in the US EV market, it’s important to consider the broader context. Tesla’s sales model differs significantly from traditional automakers, focusing on direct deliveries that are cyclical throughout a quarter, with a concentration of US deliveries occurring in the last month of each quarter.

- This model can affect how market share is perceived on a month-to-month basis. Furthermore, the overall increase in Tesla’s new U.S. registrations indicates continued growth, despite a shift in market share percentages.

- Other automakers like GM, Ford, and Volkswagen have seen increases in their shares of the EV market, thanks to new model deliveries.

- However, Tesla’s market position remains strong, and the current data may not fully reflect its ongoing dominance in the EV sector.

Economy is Reaccelerating

- On the manufacturing side, the sharp pickup in auto production, after the 4Q auto strike hit, is certainly helping.

- OEMs (Original Equipment Manufacturers), suppliers, and dealers, have reported strong results but their outlooks for the future might be too cautious.

- Solid demand for vehicles, margin recovery efforts by suppliers, show potential for upside in 2024 due to conservative estimates.

- The continuous demand on electric vehicles (EV) offers a good insight in market predictions.

- OEMs and Dealers have confidence that demand will continue to be healthy while suppliers are on their way to recover margins.

- In general, macro backdrop included in outlooks, especially volume assumptions, has been way too conservative and would expect upside through the course of 2024.

- After a long run of outperformance, P&S cooled slightly with SSS +4.9%, but is likely to continue to grow for many years ahead.

- Global production volume in focus markets is conservatively expected to decline slightly YoY, which may provide upside through the year.

- GM’s plans to resurrect PHEV technology in North America might be another sign of the slowdown of US EV demand.

- Tesla commentary was consistent with this trend, with guidance for sales growth to be meaningfully weaker in 2024.

Good finish to 2023; Expect More to Come in 2024

- The automotive industry is doing better than expected, but they’re playing it safe with their predictions.

- There’s a lot of interest in cars, especially electric ones, and this could mean more profits ahead.

- Auto companies did really well in the last part of 2023. They sold a lot of cars and made good money.

- Despite doing well, these companies are being very careful about predicting the future. They think things might not stay as good, but this could be too pessimistic.

People are still interested in buying cars, which is good news for the industry. Companies that make parts for cars are finding ways to make more profit from their sales, which helps the whole industry. More and more people want electric cars, and companies like Tesla, GM, and Ferrari are working to meet this demand.

2024 is still a long way to go, but we’re hoping with all the good economic signals that it would only bring good news and that numbers would be better than ever.