Last Updated on September 15, 2023 by Calvyn Ee

Key Points

- July continues to see minor positive improvements in car sales and inventories

- The automotive industry seems to be heading down the right track, but the UAW strike and waning consumer spending may impact overall sales till the end of the year

- EV outlook still looks positive as Tesla continues to lead and other automakers struggle to keep pace

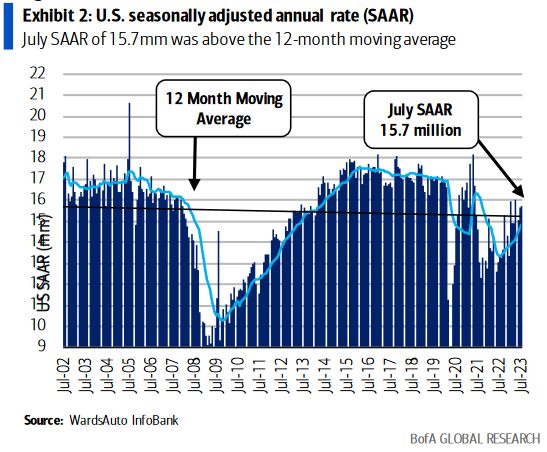

July saw another positive uptick in light vehicle sales in the United States, with a year-over-year increase of 19.9 percent and a seasonally adjusted annual rate (SAAR) of 15.7mm. While it was below the Bank of America’s “mid-month estimate of 15.9mm,” it nonetheless exceeded the year-to-date SAAR of 15.4mm. By volume, Cox Automotive does report that “new-vehicle sales were down 5.1% in July from June.”

Again, a lot of the strength in sales was supported by strong fleet performance, but it has been slowing over time. For now, fleet sales did increase by 35 percent compared to a year ago. Large rental fleets saw the most prominent increase, being up 78 percent. In contrast, commercial fleets went up by 7.5 percent, while “sales into government fleets” increased by 27 percent.

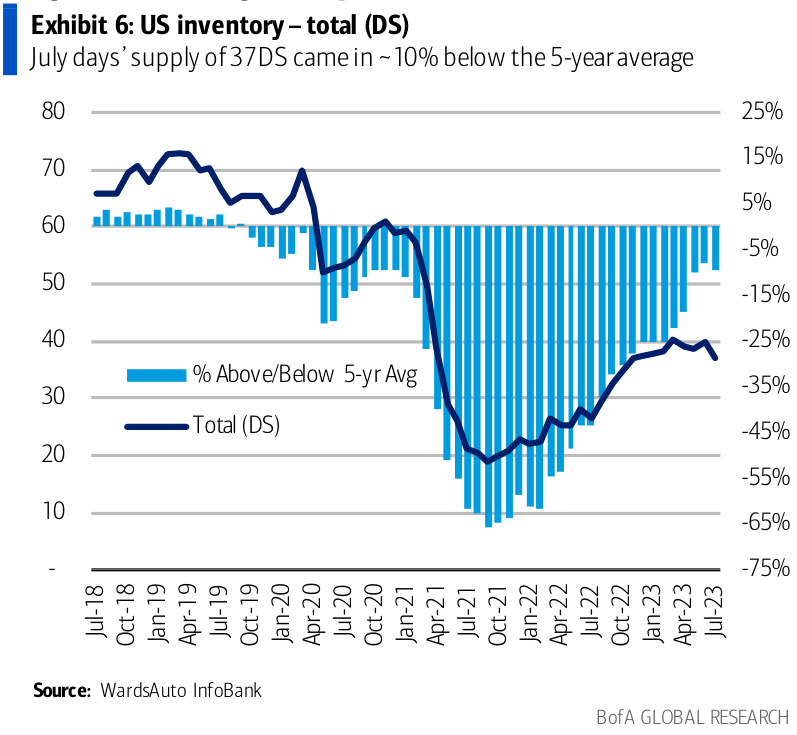

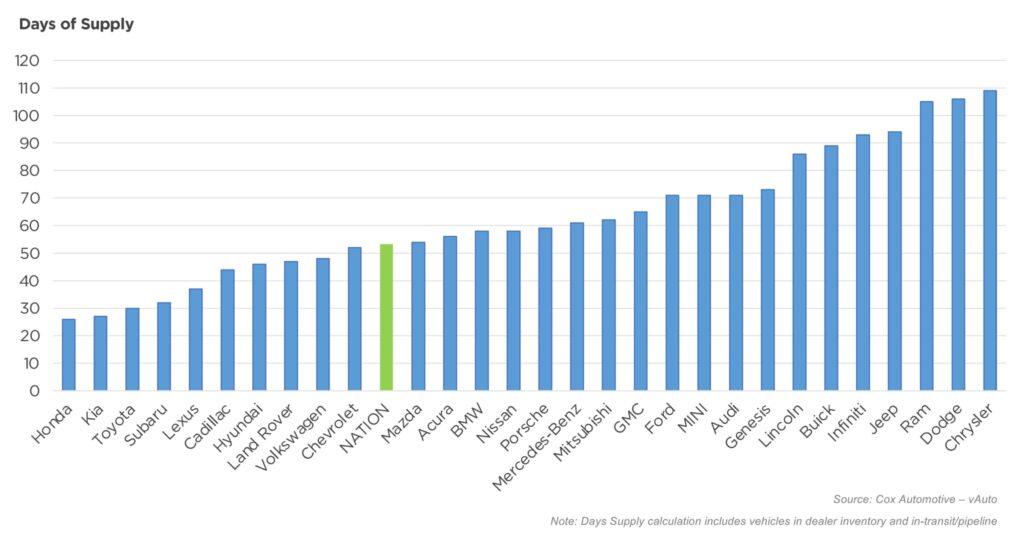

Total inventory did fall by 119,000 units at the end of July, with much of it stemming from the Detroit Three – that is, GM, Stellantis, and Ford. Honda, Kia, and Toyota continue seeing lower days’ supply than other major automakers. Inventory is currently at 37 days’ supply (DS), slightly lower than the days’ supply in June by three days. Total inventory currently stands at 1.96 million units as of July 31st. It shouldn’t be surprising that the more expensive vehicles on the market, especially luxury vehicles, have a higher inventory DS than more affordable ones.

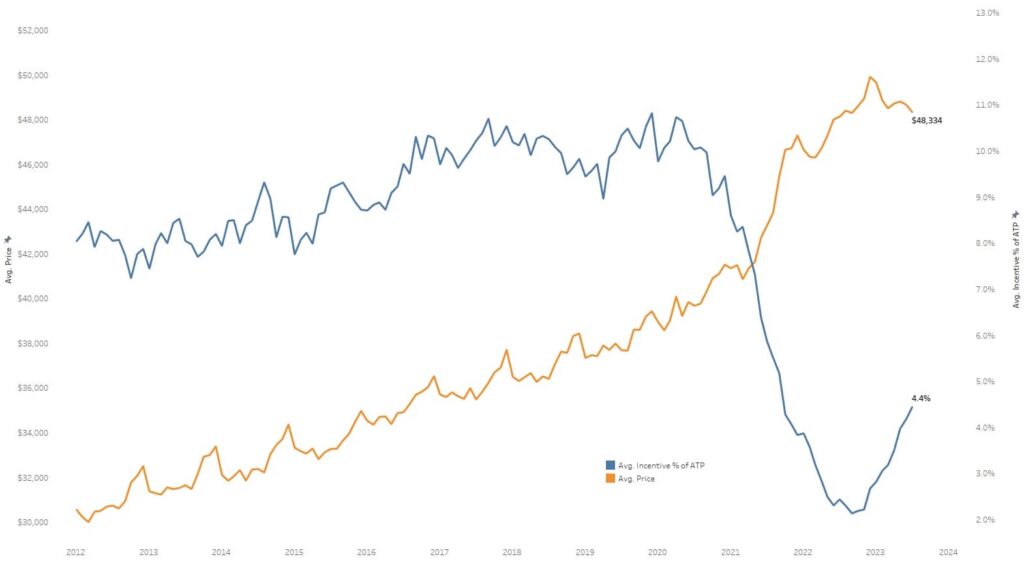

Prices are still on the elevated side despite some downward changes, with average listing prices at $47,048, a year-over-year decrease of 0.9 percent, according to Kelley Blue Book (KBB). As for average transaction prices (ATPs), KBB reports a “scant” increase of 0.4 percent, with July’s revised ATP at $48,165 – contrast this with June’s ATP of $48,671. ATPs have seen a decrease of 2.7 percent, or $1,335, marking the “largest January to July fall in the past decade.”

“New-vehicle prices, primarily driven by cuts in luxury and electric vehicles, are decreasing as inventory steadily improves. With higher inventories and higher incentives helping to keep downward pressure on prices, there certainly are good reasons for shoppers to be heading back into the market.”

Rebecca Rydzewski, Cox Automotive

Non-luxury vehicle prices have only increased by 0.5 percent year-over-year, but prices are still averaging $44,700 in June. Interestingly, only a single non-luxury vehicle has a price below the 20k mark: the humble Mitsubishi Mirage, with an ATP of $19,205 in July. Prices have fluctuated over time, but the difference has only been a few hundred dollars. On the other hand, the luxury segment saw a price decrease of “almost 3% year-over-year” at an average price of $63,552 – that’s only $192 lower than June’s figure.

Incentives also went up for the “tenth consecutive month in July” to an average of $2,148 per vehicle, or “4.4 [percent] of the ATP.” This marks the highest it’s been since October 2021.

Used Car Performance

Meanwhile, used cars also see varying degrees of fluctuations. Unsold used vehicle inventory went up from 2.21 million in June to approximately 2.25 million by the end of July; year-over-year, this marked a 9 percent decrease. Days’ supply also improved, going from 49 DS to 45 by the end of July. According to Cox Automotive, this is on par with 2019 levels, and “moderating prices and surprising summer demand may keep inventory numbers down.”

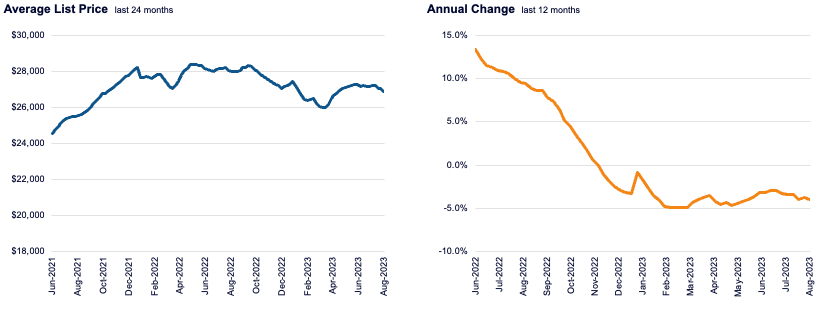

The average used car listing price reached $27,028 in July, compared to last month’s revised figure of $27,167. In fact, wholesale prices declined 1.6 percent in July from June and “were down 11.6 [percent] year over year.” The first week of August also saw the largest single-week drop in price since October 2021 at 1.1 percent. Black Book writes that “wholesale prices dropped as sellers lowered their floors and buyers were not willing to pay any more than they had to.”

Of the major automakers, Honda, Subaru, and Toyota continued to record the lowest used inventory at 38 DS for Honda and 39 DS for Subaru and Toyota. These are the only brands with DS under 40.

Overall Outlook Remains Uncertain

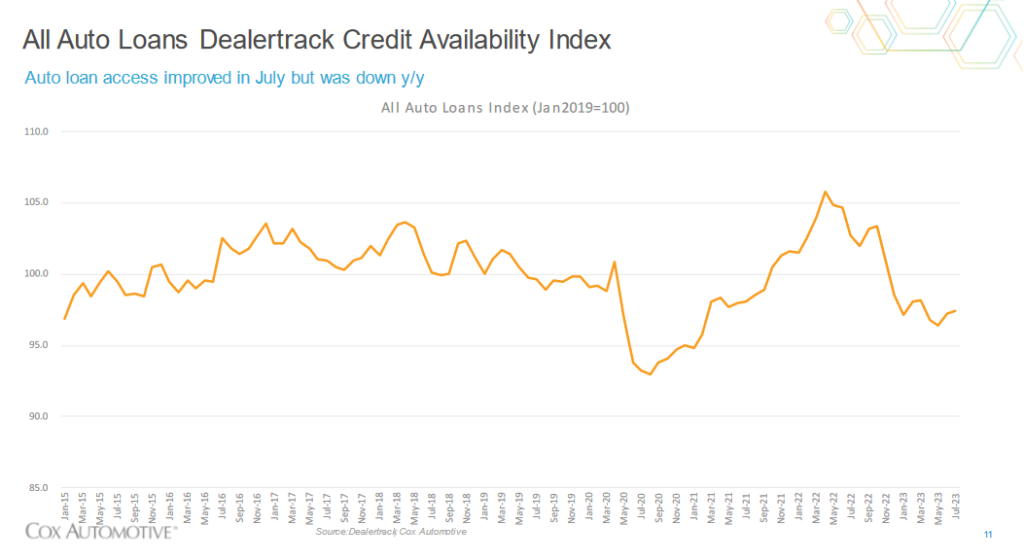

While auto loan availability improved in July, Americans are still expected to pay at least ten percent of their paychecks in auto loan repayments. In fact, it’s come to a point where owning a house and a single car costs you 45 percent of the typical American monthly budget. Despite this, higher wage gains have helped support consumer spending habits even today, including exorbitantly high auto repayments, though this trend has started to slow down over time.

Dealers are still on the losing side as their average per-sale profit dropped by 28 percent year-over-year in July, with 29 percent of dealers selling cars above their MSRP compared to 49 percent last year. As consumer spending continues to weaken and overall pricing continues its upward trend, dealers may have to face even tougher selling conditions in the future.

However, vehicle demand remains strong as more people buy new than used. Used vehicle retail sales in July are predicted to be a 6 percent increase from June, especially as attractive incentives for new vehicles and a constraint in used supply largely motivate buyers to ignore the used vehicle market.

Additionally, light truck performance continues to be strong as demand for the utility of pickups, SUVs, and crossovers stays high year-to-date. This will likely help buoy auto sales performance nationwide until discretionary consumer spending weakens substantially that funds must be diverted to more pressing expenses, such as groceries. Of course, that’s not to say that other car segments won’t sell, though they lag behind the current light truck sales figures.

The UAW Impact

The United Auto Workers (UAW) group recently appointed a new president with a more aggressive stance towards major automakers – particularly the Detroit Three – in negotiating fairer terms for auto workers – including better wages and benefits and “greater job security.” It’s been predicted that a strike is bound to happen sometime in mid-September when the UAW’s Master Agreement expires, especially if automakers are unwilling to negotiate with the UAW.

Should a strike occur, it will be a very contentious one. On the UAW’s side, strikers can “lose out on wages” that are “partially offset by the union’s striker benefits of $500 per week” if the strike becomes protracted. Automakers also stand to lose substantial profits, especially considering GM lost $3.6 billion during the 40-day strike of 2019. Meanwhile, the UAW “paid nearly $81 million in benefits to striking workers” during that strike.

Still, given their strong “balance sheets,” it’s predicted the Detroit Three will have “sufficient liquidity” to weather the strike’s effects. The Bank of America also predicts that negotiations will lead to an “approximately 25-30 [percent] increase in labor costs over the next four years” on top of “sizable cash signing bonuses” and varying “adjustments to other benefits.”

Consumer demand for Detroit Three vehicles may be impacted if there isn’t sufficient production and/or supply to meet said demand during the strike, though the Bank of America believes it won’t substantially affect the “current trend in auto sales.”

More EV Growth Expected, Despite Challenges

Experian reported a significant increase in battery electric vehicle (BEV) registrations, reaching 546,651, 62 percent more than just a year ago. BEVs accounted for 7.1 percent of the total market thus far, in contrast to last year’s 4.9 percent market share. Kelley Blue Book records that the average EV ATP was $53,469 – down slightly from June but substantially from January’s $61,000 figure.

“EV ATPs are down more than 19% from their recent peak of more than $66,000 just a little more than a year ago in June 2022.”

Cox Automotive

EV inventory remains healthy to be able to meet current consumer demand as they’re hovering around 100 DS. Incentives are also at 6.7 percent of the current ATP, amounting to $3,755, making a purchase a little more lucrative.

Tesla continues to lead in the EV race but faces challenges as other automakers step up their EV game. Of the 546,651 BEV registrations, 329,608 registrations were for Teslas – a 44 percent increase year-over-year. As for market share, it’s dipped to 60.3 percent from last year’s 67.6 percent, indicating that other companies are starting to catch up.

Tesla has had good luck in 2023, especially following price adjustments to make their offerings more attractive to buyers. In fact, Tesla just lowered the price of the Model Y’s performance and Long Range trims in China by almost $2,000 while offering insurance subsidies for 8,000 yuan (about $1,100) for rear-wheel drive Model 3s. While it’s meant to counter the 31 percent drop in Tesla sales in China from June to July, it still reflects Tesla’s commitment to increasing EV accessibility in the US and abroad.

The positive trends in EV growth might be stifled in the coming months, especially as discretionary consumer spending weakens even further. There’s also the somewhat “unenthusiastic” response from major automakers regarding transitioning to EVs. For example, Ford reduced its “target production level from 600,000 units by the end of 2023” to only 400,000 while pushing their 600k target to next year. Meanwhile, GM took up “a nearly $800 million charge” to account for the Chevrolet Bolt’s recall due to battery fires.

The Bank of America’s predictions of “tougher pricing, higher expenses, and lighter demand” in the latter half of the year may not necessarily come true, especially if EV prices continue this downward trend. The existence of budget-friendly options like the highly-popular Chevy Bolt – currently the most affordable option available to buyers – and the Nissan Leaf will be catalysts to drive demand up further. GM’s decision to reverse the Chevy Bolt’s discontinuation may pay dividends even as they offer pricier options (like the Chevy Silverado EV) for their more affluent customer base.

Tesla is still pushing hard to stay ahead of the game, but competitors are already catching up through price wars, innovation, or a mix of both. Price wars are still ongoing in the wake of Tesla slashing prices, as even Lucid, makers of the luxury Air EV model, has reduced prices on its top trims (as much as $12k on its Touring and Grand Touring models) to compete. It doesn’t necessarily equate to long-term success, especially with Tesla’s outstanding lead over the competition, but it can help keep demand going.